The “15/3” credit‑card trick (also called the “15/3 rule” or “15/3 hack”) is a timing strategy some people use to try to improve their credit score faster by making two payments each billing cycle: one 15 days before a key date and another 3 days before that date. There are two common versions of the trick:

- Version A (due‑date version): make one payment 15 days before your payment due date and another 3 days before the due date.

- Version B (statement‑closing version): make payments 15 days and 3 days before the statement closing date (the date the issuer locks the balance they report to credit bureaus).

Both versions aim to lower the balance that the card issuer reports to the credit bureaus — i.e., to reduce reported credit utilization — which can help your credit score. However, the specific 15 and 3 day numbers are arbitrary and the method is often misunderstood. Read on for what actually matters, real advantages, limitations, and better alternatives. (SoFi)

How credit reporting and utilization actually work (the facts you need)

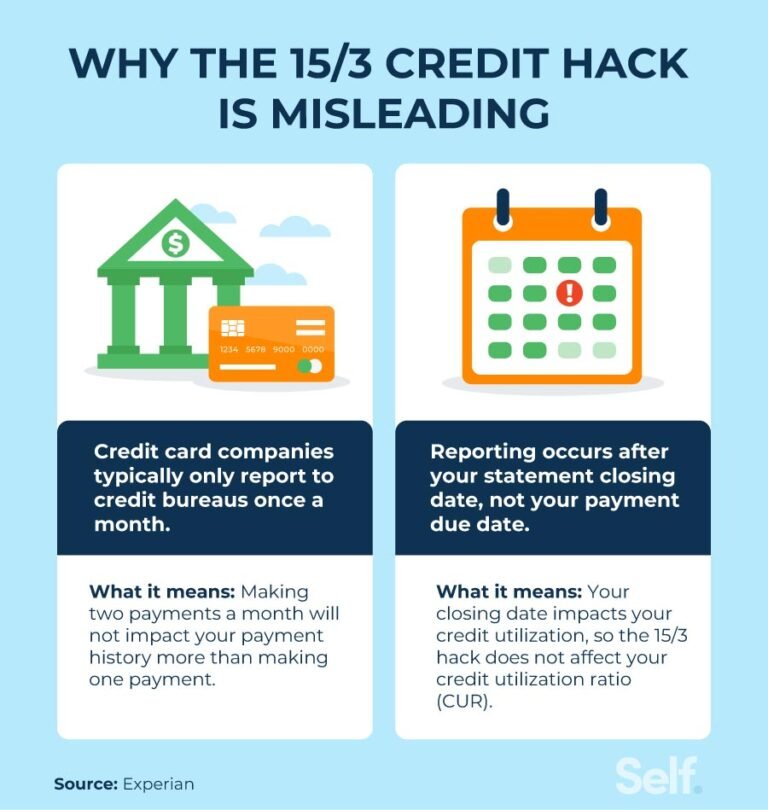

- What gets reported: credit card issuers generally report the balance on your account to the credit bureaus around the statement closing date (not the payment due date). If you want the lowest balance on your credit report for that cycle, you must lower your balance before the statement closing date. (Experian)

- Utilization matters numerically: credit scoring models pay heavy attention to credit utilization (balance ÷ credit limit). Many experts recommend keeping utilization under 30%, and preferably under 10%, on each card and overall to maximize score benefit. Reducing the reported utilization helps your score. (SoFi)

- Number of payments ≠ number of reports: making multiple payments in a month does not make the bureaus receive multiple “reports.” The bureau sees whatever balance the issuer reports at the reporting date. Multiple payments can lower the reported balance if they occur before the closing date, but paying 15 days and 3 days before the due date will often be too late to affect that month’s reported balance. (Nasdaq)

Why some people use 15/3 (and where the idea came from)

- The trick spread on social media and personal‑finance blogs as an easy calendar rule: “pay once mid‑cycle, pay again just before the end.” It’s simple to remember and creates a built‑in safety net to avoid late payments. That simplicity is part of its appeal. (FinMasters)

What actually works (practical, verifiable takeaways)

Short checklist (truthful, actionable)

- Find your statement closing date. That’s the single most important date to know if your goal is to lower reported utilization.

- Pay down your balance before the statement closing date (not the due date) to reduce reported utilization. A single well‑timed payment before closing is sufficient. (Experian)

- Aim for <30% utilization, ideally <10% on each card and overall, for the best score impact. (SoFi)

- Automate or calendar reminders if you struggle with dates — consistency matters more than which specific days you pick. (I Will Teach You To Be Rich)

Advantages claimed for 15/3 — and the truthful assessment

| Claim | What’s true |

|---|---|

| “It boosts your credit score fast.” | It can help if those payments lower the balance reported at statement close. But the specific 15 and 3 day spacing is arbitrary — lowering the reported balance is what matters, not the 15/3 numbers. (SoFi) |

| “It prevents late fees.” | Making two payments creates redundancy and can reduce late payments — true. Splitting payments across the month is a valid behavioral strategy to avoid missed payments. (I Will Teach You To Be Rich) |

| “Multiple monthly payments increase reporting instances.” | False — credit bureaus typically get one balance per account per cycle from the issuer. Multiple payments only help if they reduce the balance before reporting. (Nasdaq) |

Numerical examples (illustrative)

Assume: credit limit = $5,000, monthly charges = $1,500.

- No pre‑closing payment — issuer reports $1,500.

- Reported utilization = $1,500 / $5,000 = 30%.

- Single pre‑closing payment of $1,000 (paid before closing) — issuer reports $500.

- Reported utilization = $500 / $5,000 = 10%. Big improvement.

- 15/3 payments but paid after closing (too late) — reported balance still $1,500 (30%). No benefit to reporting.

Lesson: the timing relative to the statement closing date is what changes the reported utilization number — not whether you paid on day 15 and day 3 of anything. (Nasdaq)

Downsides or misunderstandings to watch for

- Overstated promises: several reputable sources call the “hack” misleading because the arbitrary 15/3 days themselves are not magic. Don’t expect huge score jumps just by following 15/3 unless you actually reduce reported utilization. (NerdWallet)

- Timing mistakes: many people target the due date instead of the closing date, which often produces no change to the reported balance for that cycle. (Nasdaq)

- Behavioral cost: making lots of micro‑payments can be time‑consuming; automation or one strategic pre‑closing payment is often simpler and equally effective. (I Will Teach You To Be Rich)

Better alternatives and comparisons (table)

| Strategy | Effect on reported utilization | Ease | When to use |

|---|---|---|---|

| Pay before statement closing | High — directly lowers reported balance | Easy (1 payment) | Best single tactic to lower reported utilization. (Experian) |

| Request higher credit limit | Lower utilization by increasing denominator | Medium (requires approval) | Great when you qualify; immediate utilization drop if approved. (SoFi) |

| Make multiple payments (15/3 style) before closing | Works if all payments are before closing | Medium (more manual) | Useful if you’re paid mid‑month and end‑month; good safety net. (FinMasters) |

| Open small installment/credit-builder loan | Adds installment account → can help score mix over time | Medium | Use when you need to build credit mix; not a utilization tool. (creditleveragex.com) |

| Automate one payment timed before close | High (same as paying before close) | Easy (recommended) | Best balance of effectiveness + low effort. (I Will Teach You To Be Rich) |

Step‑by‑step: a practical, tested routine

- Find two dates for each card: (A) statement closing date and (B) payment due date. (Most issuers show both on your online statement.)

- Set an automatic payment for a substantial payment 3–5 days before the statement closing date (this ensures the bank records the payment in time). If your paycheck arrives mid‑month, schedule that payment accordingly. (Experian)

- Optionally make a small “safety” payment 3 days before the due date to avoid late fees (this is the behavior the 15/3 rule encourages). But again: that second payment won’t change the reported balance for that statement if it occurs after closing. (Nasdaq)

- Aim for target numbers: <30% is a minimum; <10% reported utilization is a stronger target for score improvement. (SoFi)

Common myths — busted

- Myth: “Doing 15/3 guarantees a higher score.” → Busted. It only helps if it lowers the balance the issuer reports at closing. (NerdWallet)

- Myth: “Issuers report daily.” → Usually false. Issuers typically report the balance as of the statement close once per cycle. Exceptions exist, but they’re uncommon. Check your issuer’s reporting practices if you’re unsure. (Nasdaq)

Useful (verifiable) resources and further reading

- Experian — Does the 15/3 Credit Card Hack Work? (clear primer on reporting and myths). (Experian)

- SoFi Learn — 15/3 Credit Card Payment Method: What It Is & How It Works (practical explanation). (SoFi)

- NerdWallet — The ’15/3′ Credit Card Hack Is Nonsense (analysis and what to do instead). (NerdWallet)

- Nasdaq (opinion/analysis) — Can The 15/3 Credit Card Hack Save You Money? (debate and expert quotes). (Nasdaq)

- FinMasters — detailed explainer and variants of the 15/3 approach. (FinMasters)

Bottom line (short and honest)

- The real objective is to lower the balance reported at the statement closing date, because that’s what affects utilization and, therefore, much of your credit score.

- The 15/3 trick is a memorable schedule that can help people avoid late payments and — if timed relative to the statement close — reduce reported utilization. But the specific “15 days and 3 days” are arbitrary and not inherently magical. Treat 15/3 as a behavioral aid, not a guaranteed hack. (Nasdaq)